European macro outlook: France reform agenda aids bullish Eurozone growth, Italian elections undermine Euro

Sentiment in Eurozone risk assets has improved. Macron’s pro-EU and pro-growth reform agenda and EU regulators’ swift intervention to deal with weak lenders and bad loans are a major driving force to sustain it. A softer version of UK’s exit from the EU also means UK risk sentiment should stay upbeat as uncertainty over trade and capital flows is reduced.

A stabilising Euro, Sterling and banking sector underpins a resilient outlook for Eurozone and UK equity markets. Against this backdrop a select equity exposure emphasising stocks of quality and growth, along with small-caps, may be considered by investors. The focused style strategies also may shield investors to global macro risks pertaining to expectations of Trump’s reform agenda, Fed tightening, crude oil volatility and China’s soft-landing better than large-cap biased broad equity markets in general.

Further out, we are cautious on the outlook for the Euro as Italy has yet to hold parliamentary elections. Italy’s status quo of low growth and high unemployment means fringe parties could still seize the initiative in coalition forming and destabilise the government, souring risk sentiment and undermining the Euro. We believe overseas investors should consider hedging their Eurozone equity exposure as election day closes in: potentially in the fall this year, but more likely in early 2018.

Longer term, a structurally weakened UK economy may also trigger more volatility and increased downside risk. It leaves room for inflationary pressures to build up as the BoE considers delaying tightening monetary policy. Hedging gilt exposure may be warranted.

Eurozone: growth momentum contingent on France’ structural-led reform agenda

Most of Europe’s political uncertainties overhanging the Euro are—for now—over. The Dutch voted for preserving the status quo, endorsing the Liberal democrats to lead another coalition government, which while yet to be formed will likely comprise of a mixed bag of left, centre and right-leaning conservative and progressive parties. The German elections in September will be a non-event: Chancellor Merkel faces Martin Schultz as her strongest opponent, both of whom are staunchly pro-European.

The potential game changer in Europe has been the French elections, however. In securing an absolute majority in parliamentary elections, President Macron has a real chance to push through his pro-growth reform agenda—by decree if necessary. It presents the best possible political outcome to reinvigorate the long-term growth trajectory for not just France, but also for the Eurozone in general.

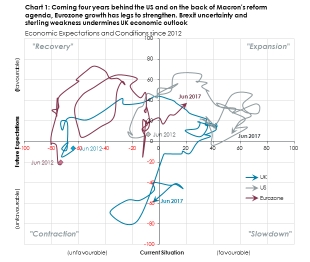

The current stage of the economic cycle, showcased in chart 1, suggests the Eurozone economy has legroom to strengthen. Given the tendency of economic expectations to lead current economic conditions by several months, survey based data show that with a near term economic outlook steadily improving, Eurozone GDP is expected to strengthen on the back of it. For this to be sustained longer term, it is largely contingent on Macron succeeding in deregulating its labour market and promoting EU-wide fiscal stimulus. A France-led domestic-demand growth agenda reinvigorates the long-term growth trajectory of Eurozone GDP to more closely resemble that of the US, now in its fourth year of robust expansion.

Importantly, a Eurozone consumption and investment-led growth trajectory would sustain the recovery much better than the export-based recovery since the aftermath of the financial crisis which was a result of a cyclical rebound in overseas markets and above all, Germany-led. This lopsided recovery sits on vulnerable foundations as the picture of global trade is clouded by protectionist rhetoric by US President Trump, weak commodity prices and China’s ability to soft-land the economy without short-circuiting investor confidence. Moreover, having already reached near full employment major real wage gains unseen elsewhere in Europe, Germany is unlikely to “lift” Eurozone growth beyond what is has already contributed. Instead, the onus will be on France’s Macron-led new government to boost jobs at home and take the investment initiative to the EU to sustainably improve the Eurozone economy.

Source: WisdomTree, Bloomberg.

Data points based on diffusion index of ZEW surveys on economic conditions

UK: Sterling slump hits outlook for consumer-led growth

Downbeat is the outlook for the UK where economic sentiment has soured around the uncertainty that Brexit has created for trade, investment and Sterling. Post the EU referendum in June 2016 and up until the end of 2016, businesses frontloaded their spending to lock in working capital requirements and secure near term trade deals. Subdued inflation and ultra-cheap credit also propelled consumers to spend, driving UK GDP growth on the back of it. Now, having come with a considerable lag, a sharply devalued Sterling is inducing import-led inflationary cost pressures onto consumers and undermining their propensity to spend further out. Beyond manufacturing, the devaluation has done little to nothing to improve UK’s trade deficit which, because of its services-bias is more prone to competitive pressures stemming from losing EU passporting rights. The result is a considerable weakened outlook that has yet to feed through into current economic conditions.

Short term, the increased probability of a soft-Brexit will work to sooth investor sentiment around Sterling. However, the growing imbalance of the UK economy, ever more dependent on foreign capital to finance the trade deficit, is structurally weakening the pound longer term. Against the backdrop of debt-fuelled spending, the BoE is likely to delay or slow tightening as much as possible, allowing inflationary pressures to seep through even as the Treasury will be incentivised to keep fiscal policy accommodative. The prices of Long-dated government bonds, yielding well below inflation, look vulnerable against this backdrop.